The movement of money is undoubtedly the most constant element of any house buying or selling process. Earnest money and down payments are two major components of facilitating the close of properties, but they can often get confused.

In this article, we are taking a look at some of the key similarities and differences between earnest money and down payments in real estate. Understanding key distinctions in both tools helps you have a better chance to land a deal with a seller of a property and positions you to have potentially smaller back-end costs in the housing process.

Let’s give some background to start.

What is Earnest Money?

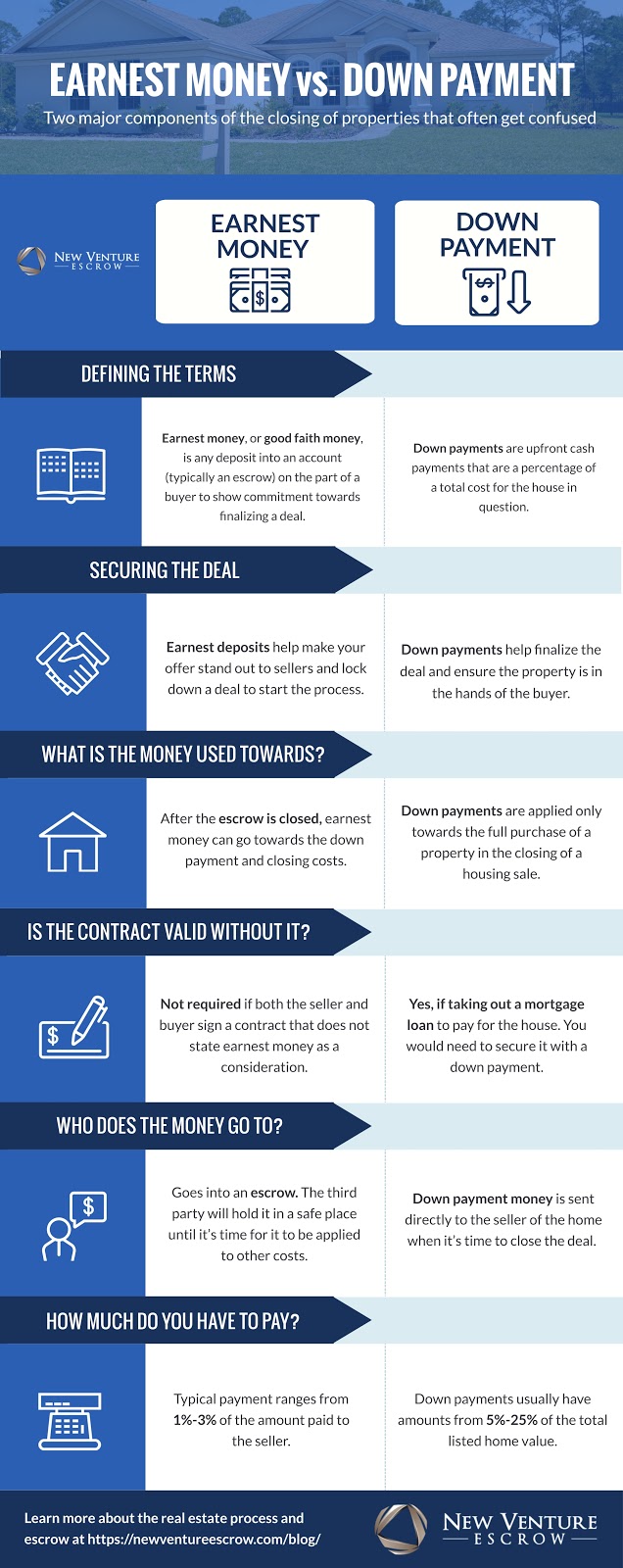

Earnest money, or good faith money, is any deposit into an account (typically an escrow) on the part of a buyer to show commitment towards finalizing a deal.

Offers come in waves from many potential buyers, so sellers are not usually keen to go begin a deal with someone who doesn’t have the full intention to purchase the house from them.

While earnest money is not a requirement for most housing deals, making that payment is a big boost that sets a buyer apart from the others. The money produced in earnest money real estate kickstarts the escrow process for both the buyer and seller.

Promissory Notes

For the purpose of showing commitment, buyers can try an alternative method – a promissory note. Promissory notes are letters of intent, stating that the buyer has strong interest in completing the sale of the property in question.

Promissory notes aren’t always effective, as there is no cash deposit involved with their submission to a seller.

There are several cases that make earnest money both refundable and non-refundable. The most common fate for good faith money is to go directly to closing costs and other expenses in a completed deal.

In cases where the deal may fall through, certain earnest money contingencies can be put in place beforehand to make sure that deposit is returned.

What is a Down Payment?

Down payments are upfront cash payments that are a percentage of a total cost for the house in question.

The average down payment for a house in California ranges from 3% minimum to about 20% maximum. The reason is that 3% is typically the absolute minimum you can put down in order to qualify for a mortgage.

In many cases, down payments are the remainder that buyers will have to pay out of pocket to complete any deal in progress due to financing options that are available to them.

Money used as a down payment does not come back to the buyer, as it is needed to pay for the listed price of the property set by the seller. Don’t expect any reimbursement when down payments are submitted!

Down payments are necessary to the closing of the housing sale process, so there is no alternative when money is needed to complete the deal and get the keys to the property.

Securing the Deal

The biggest shared benefit between earnest money and down payments is giving the buyer the means to progress with housing deals. Earnest deposits help make your offer stand out to sellers and lock down a deal to start the process. Down payments help finalize the deal and ensure the property is in the hands of the buyer.

Both are needed in making sure the property you are interested in becomes yours at the end of the process.

What is the Money Used Towards?

One of the main differences in earnest money vs. down payment lies is what they go towards, respectively.

Earnest money is the tool used to begin the escrow process for sellers and buyers. There is a common question that people ask:

Does earnest money go towards down payment or closing costs?

At the close of any escrow account, the money deposited can go towards the down payment and closing costs to help wrap up the entire deal.

Down payments are applied only towards the full purchase of a property. Those funds are solely for the closing of a housing sale and don’t go towards other things.

Who Does the Money Go To?

When discussing earnest money vs. down payments, another key difference is where cash from each ends up in the closing process.

Money that is designated for earnest payment goes into an escrow from the time an account is open to the close. Once that money is put up, the third party will hold it in a safe place until it’s time for it to be applied to other costs.

Down payment money is sent directly to the seller of the home when it’s time to close the deal.

How Much Do I Have To Pay?

There is no concrete amount that anyone would have to pay for both mentioned modes of payment for housing deals. However, both have common ranges of money amounts that most people adhere to in house deals.

For earnest money, the typical payment in California ranges from 1%-3% of the amount paid to the seller.

Down payments usually have amounts from 5%-25% of the total listed home value. A major component that goes into these payments is the proportionate amount of interest that is paid at a later time. In essence, the more you deposit in the down payment, the less monthly mortgages will be for financing options post-sale. See the infographic below and DOWNLOAD YOUR OWN COPY HERE!

Want to Know More About the Escrow Process?

If you are putting down earnest money for a house in California, you’ll need an escrow account to keep your funds secured. Please get in touch with us at New Venture Escrow and we’ll answer any questions you may have. Whether on the buying or selling side, we have experts that are ready to make your escrow experience as seamless as possible.

Be sure to take a look at all of our resources to get in-depth information on all things escrow.