It’s pretty common knowledge that a lot goes into buying a new home – mentally, emotionally, physically, and financially. For most people, it is one of the most important steps they will take in their adult life.

In 2020, our nation’s economy took a staggering blow due to the COVID-19 pandemic. Slowly but steadily, we have regained footing as life starts to become normal again. There has hardly been an area of the economy that has remained untouched by the effects of the virus. However, in terms of the housing industry, we have seen a surprising rapid increase in sales and mortgage credit availability.

Why is that?

Qualifications to certify for a mortgage rate have been exceedingly stringent in the past. This means that qualifying was difficult for those without a good credit score. The younger generation of new home owners was most affected by these conditions, for reasons that include a lack of a steady job, student loans, debt, and credit scores yet to be built up.

However, we have good news! If any of the descriptions above apply to you, qualifying for a new home will be easier now more than ever!

The Current Real Estate Market in the U.S.

In 2021, housing prices have rapidly increased, with recent data showing this trend will most likely continue in early 2022. A rapid increase in demand coupled with low supply has led to a 29% sale increase above the listed price. Data from early this year also shows that annual value growth has climbed to the highest it has been since 2005, coming in at 11.6%.

Basically, the housing market in the US is more competitive than it has been in over a decade. For example, in San Diego, real estate is booming as investors are flocking to buy a piece of real estate.

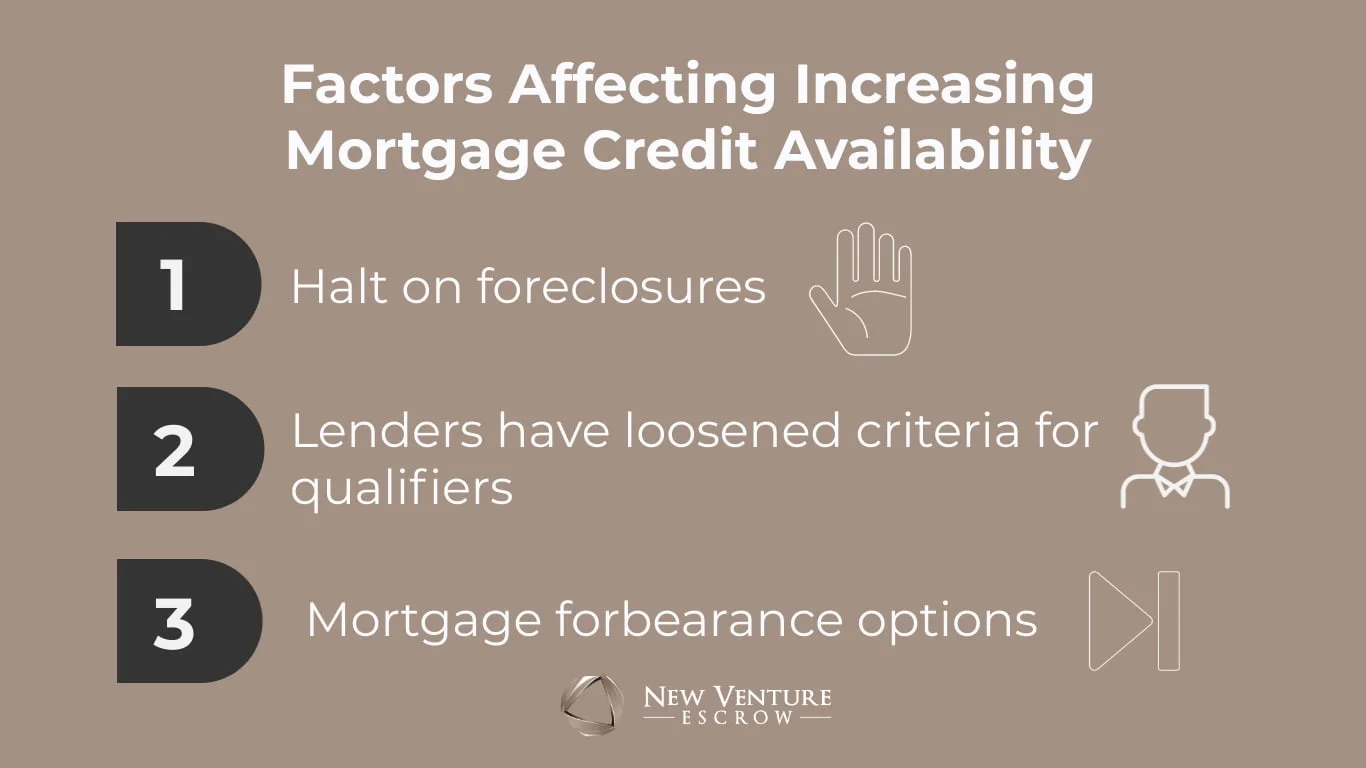

In terms of mortgage rates and credit availability, most lenders have dramatically cut back on their previous strict criteria for qualifiers. The pandemic opened a door for those who would typically receive a rejection, such as the demographic of young, first-time buyers.

There isn’t much standing in the way of those wanting to purchase a new home. Foreclosure bans and mortgage forbearance options are still in play, also playing a major role in the low supply of homes. Take a look at this article to learn more about the halt on foreclosures, and how the industry has been affected by it.

What Does This Mean for New Homeowners?

With mortgage criteria more lax than ever, and with credit availability steadily rising, new home owners will benefit the greatest from this housing explosion. The only issue buyers may have is finding a house to buy!

As if the odds weren’t enough in their favor, first-time buyers will be happy to hear of a new legislation coming into play. Under the Biden administration, a $15,000 tax credit will soon become effective, specifically for those who are buying their very first home.

Not only is this bill undergoing transition into legislation, but a new grant called the Downpayment Toward Equity Act of 2021 is also underway. This grant calls for $25,000 in cash for first-time purchasers, allowing them to use this credit towards housing, mortgage interest rates, and closing costs. Neither of these acts have come into play as of yet, but our presidential administration has made steady moves towards sealing these deals into laws.

Am I saying that thanks to COVID-19, what is usually a stressful and strenuous situation in the field of buying and selling houses, it has now never been easier?

Yes, you had better believe it!

The housing market is finicky, prone to changing, and constantly diverse. However, the future looks bright these days for those who have never purchased a home before. Although the COVID-19 pandemic dealt us all a hard blow, it has also created a light at the end of a tiring tunnel, making it more seamless than ever for first-time buyers.

We’re here to help with all your real estate needs and questions! For further information and updates on buying, selling, and the latest trends in real estate, visit our New Venture Escrow blog page.