Attention all California home sellers – we’re here to help you quickly and painlessly understand how the home closing process works in California and what costs you should expect to incur. In this article, we’ll cover the following questions:

- How does closing on a house work?

- How much are closing costs?

- Who pays for closing costs?

- What are the common closing costs for sellers in California?

How Does Closing on a House Work?

Imagine Jim is selling his home in California (hurray!). He bought a property for $300K and ten years later is selling it for $500K. Great turnaround, Jim!

He is finally ready to close on the property, meaning that all money and documents are ready to be sent so that Jim can transfer ownership to the new buyer and receive the money.

The closing of Jim’s property is facilitated by a third party escrow company to make sure all of the documents and monetary funds are transferred safely.

Jim is ready to walk away with full pockets… but not so fast, buddy.

Like so many others, Jim is under the impression that the home closing process for sellers is as simple as receiving an offer and walking away with a sweet ROI.

In reality, there are several closing costs that sellers will incur during the final sale (closing) of their property.

Keep reading, California sellers, to prepare yourself for the money you’ll actually be making in the real estate closing process.

How Much are Closing Costs?

According to Realtor.com, the fees paid to third parties can amount to 2%-7% of the final sale.

Jim, for example, would pay anywhere from $10,000 to $35,000.

Check out this homesale calculator to help determine the costs around your specific situation.

Who Pays for Closing Costs in a Real Estate Transaction?

The contract drawn up around the purchase will determine which party incurs which closing costs (buyer or seller).

In the state of California, however, there are different county standards that determine who pays which closing cost.

For example, in Alameda the buyer is expected to pay the escrow fees, whereas in Alpine the buyer and seller split the escrow fees. Discover the division of closing costs by county in California so you can anticipate what you’ll be expected to pay.

What Are Common Closing Costs For Sellers In California?

Regardless of whether you decide to sell your home through a real estate agent or go about it FSBO (for sale by owner), there are mandatory closing costs associated with the sale of your home which includes:

- Title insurance fees

- Title search

- Escrow fees

- Transfer taxes

- Prorations for property taxes

- Agent fees

- Miscellaneous fees

What Are Title Insurance Fees?

Both buyers and sellers usually obtain title insurance in the case that they incur title problems, such as forgeries, undiscovered wills, or illegal deeds.

The average cost of title insurance for a California home purchase is $544, according to ValuePenguin.

What Are Title Search Fees?

A title search must be executed in order to prove you are the rightful owner of your property and have no outstanding claims or judgments.

The official title search will usually set you back $150-$250 and can be conducted completely online.

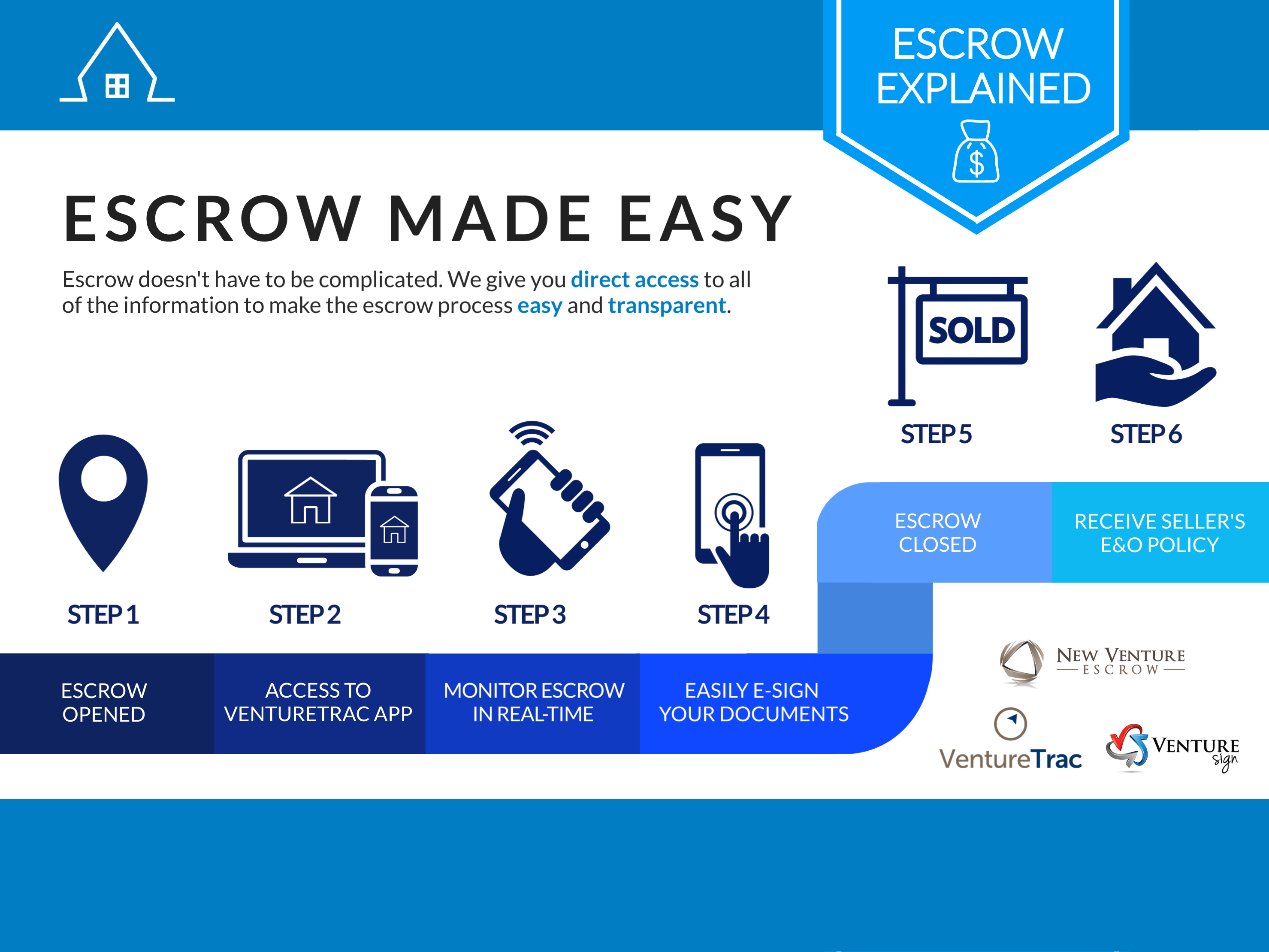

What Are Escrow Fees?

In California, an escrow service is a standard feature of real estate transactions. The entity functions as an independent third party that holds all of the relative documents (often in the hundreds) and money in a safe place until the closing of the sale.

Our home seller Jim, the owner of the property, would transfer all the documents to the escrow agent. The agent would then hold all of Jim’s documents in one place until the buyer transfers the money for the sale. The escrow company then ultimately transfers it to the seller.

A rough calculation of escrow fees in California usually comes out to $2 per $1,000 of the property, plus $250. On Jim’s $500,000 property, he might pay [($500,000/$1,000) x $2] + $250 = $1,250.

Having an escrow company that allows you to e-sign and track your documents step-by-step is extremely useful for home sellers. Jim keeps all his paperwork in order using New Venture Escrow.

Check out the complete list of the documents needed to sell a home – you might want to sit down for this one!

What Are Transfer Taxes?

Transfer taxes can be imposed on home sales by county, city, and HOA. Let me explain.

The California Documentary Transfer Tax Act allows counties in California to charge 55 cents per $500 of the property value ($1.10 per $1,000). Not all counties enact this right, and the state average for California is $750.

Not all cities have transfer fees, but they can enact their own tax rates. In Berkeley, for example, the transfer tax rate is $15 for each $1,000.

HOA transfer fees can fall anywhere between $100-$400.

If Jim is selling his $500,000 home in Berkeley, a particularly expensive city, then he is susceptible to $550 + $7,500 + $400 = $8,450.

Want to avoid documentary transfer tax? In California, home sellers can seek exemptions if their home sale falls under the following categories:

- Writings to secure a debt

- Transfers incident to reorganizations or adjustments

- Transfers of interests in entities taxed as partnerships

- Transfers to or from governmental entities

- Transfers that only reflect changes in the method of ownership

- Transfers pursuant to divorce or separation

- Transfers by gift or death

If you think you are eligible for an exemption, consult your real estate agent to know more.

What Are Prorations for Property Taxes?

Assume Jim moves out of his house at the end of September and the new homeowner moves in at the beginning of October.

The property taxes for that year will fall proportionally (not equally) on the two owners, meaning Jim will have to pay more because he was living in the property longer.

The daily tax amount will be multiplied by the number of days each homeowner was in the property. This number depends on the property taxes of your home.

What Are Agent Fees?

This is the amount of money the seller pays to the real estate agents involved.

Depending on the contract, the listing agent would make 2.5-3% of the final sale, and the buyer’s agent would make 2.5-3% of the final sale.

That can be up to 6% of Jim’s $500,000 property, amounting to $30,000. These fees are often split between the buyer and the seller.

What Are Miscellaneous Home Closing Fees?

Depending on the specific home sale contract, the seller can incur the following miscellaneous fees:

- Termite inspection (~$75-$150)

- Home inspection (~$200-$400, depending on the size of the home)

- Natural hazard disclosure report (~$100)

- Relevant repairs (agreed upon in the contract)

- Home appraisal ($450-$650)

There are also the personal costs of moving furniture and goods.

Make Sure You Are in Good Hands for the Biggest Transaction of Your Life

Closing on a home is often the biggest transaction people make in their lives. Make sure you’re in good hands with a transparent California escrow company that allows you to e-sign documents and keep track of the progress of your escrow every step of the way.

Get in touch with an agent today and see how New Venture Escrow can help.