Let’s tackle the crucial factor in the home buying process – money! Mortgages and interest rates are the big buzzwords when discussing your options and potential costs. But what exactly does that mean?

A mortgage is any type of loan that is used to purchase or refinance a house. When you have a mortgage, interest will follow.

At the time of closing on your home, you will receive the parameters of your interest rate. It will be incorporated into your monthly mortgage payment. Interest really can’t be avoided if a loan is involved. However, the major influence on the level of interest rates comes from both the economy and a borrower’s financial well-being.

Why Should You Understand Mortgage Interest Rates?

Mortgage interest rates are volatile! They can change drastically on a day-to-day basis. Be aware of the factors that can increase or lower interest rates. Even a small improvement can save you significant amounts of money over time.

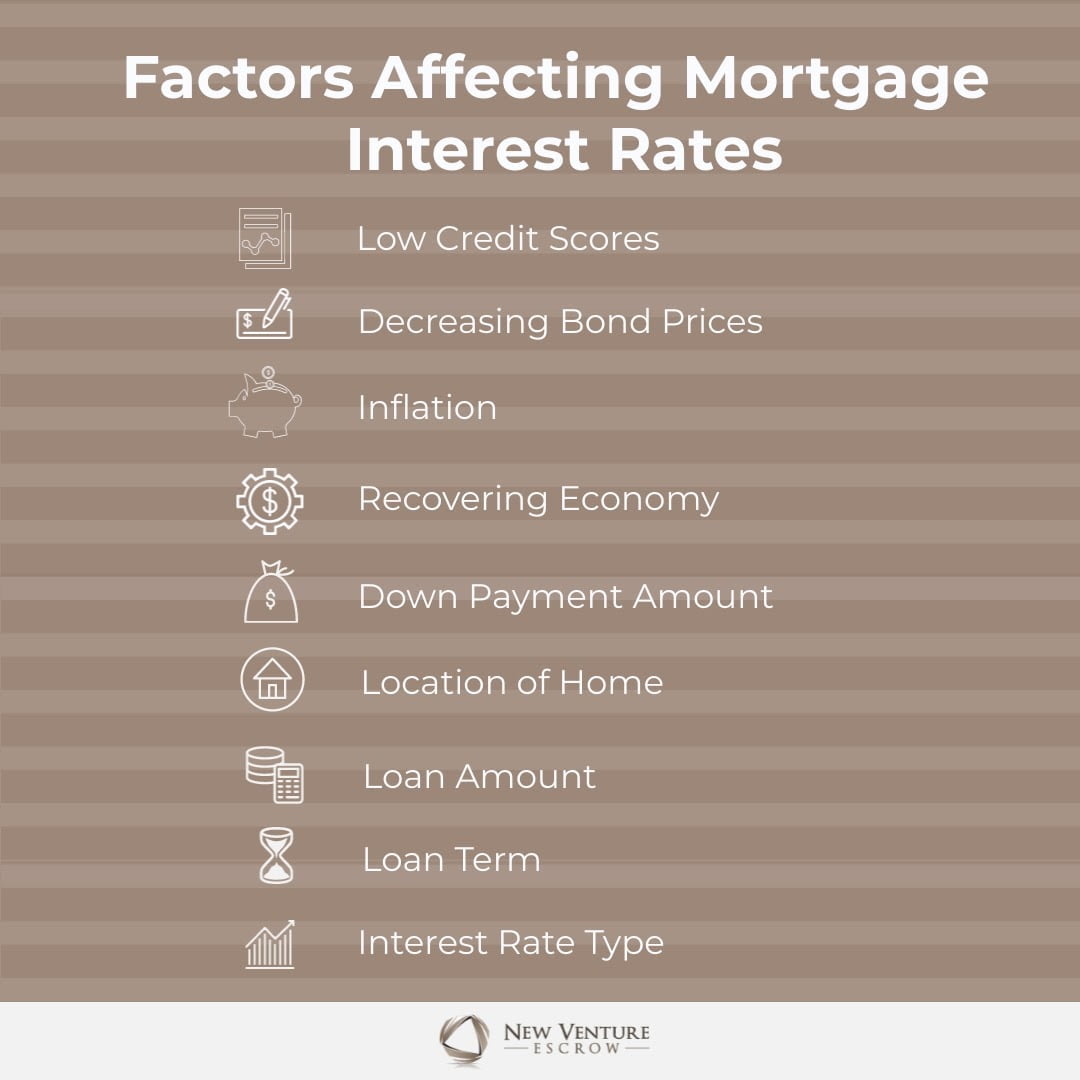

Current trends show rising interest rates in the economy. Check out the factors affecting mortgage interest rates so you can be aware of when to buy, and decide how to proceed with your home purchase!

1. The Economy

The current performance of the economy, both nationally and globally, impacts interest rates. Basic economic principles such as supply and demand play a major part in the price structure of your mortgage payment.

For instance, a strong economy means rising interest rates in most cases. You can prepare by reviewing political news and market reports.

2. Bond Market Prices

Bond prices have a complicated economic connection to mortgage interest rates. Mortgage interest rates are inversely related to bond prices. When bond prices decrease, interest rates rise. On the other hand, when bond prices increase, mortgage interest rates decrease.

3. Inflation

Inflation is another critical factor for mortgage lenders. If inflation increases, then everything else must keep up to match. High inflation in the country means higher interest rates on your mortgage payments.

4. Personal Credit Scores

Your financial health is one of the most important factors affecting interest rates. Your credit score is a metric of your ability to uphold your end of a financial agreement. Credit scores demonstrate your reliability.

When you have a high credit score, you typically can receive a lower mortgage interest rate. The first step to take is to check your credit as early in the home buying process as possible. Review your credit report and identify any errors or improvement avenues. It takes time to correct errors and boost your score.

5. Down Payment

A down payment is the upfront, cash amount that is paid at the time of a home purchase. This money will not be returned to the buyer. Down payments can be negotiated in certain home transactions, so there may be some ability to influence the impact on your future mortgage interest rate.

A larger down payment usually results in a lower interest rate because a higher down payment reflects a strong financial commitment to the purchase. If you can provide more money upfront, that signals security to the lender and they will examine your interest rate accordingly. If it is in your budget to do so, consider raising your down payment to 20% of the home price.

6. Location of Home

Mortgage rates are different throughout the country! Your state may have higher interest rates than others. On a smaller level, your city or county could play a role too. There may be more competition in trending areas between local lenders. Select loan types are contingent upon location as well.

7. Loan Amount

The principal loan amount and house price influence interest rates. This one is less straightforward, but a large loan or even a small loan can mean higher interest rates. The key is to select a home price that fits right in your reasonable budget.

8. Loan Term

The duration of your loan is important for your interest rate. There are many variables that create your monthly mortgage payment, but shorter loan terms typically result in lower overall interest rates. You may need to do some calculations to see what the impact is if you shorten your loan term.

9. Interest Rate Type

Interest rates vary by type of mortgage. There are two main types that have clear-cut interest rate implications – fixed or adjustable. Fixed interest rates are set and will not change over time.

An adjustable mortgage can change. For a portion of the loan term, the rate may be fixed, but after a certain point in time, the rate becomes subject to the conditions of the market.

More Tips for New Home Buyers or Sellers

Understanding the factors influencing interest rates is just the first step on your journey. Get in touch with experts at New Venture Escrow for guidance on your home buying or selling process!